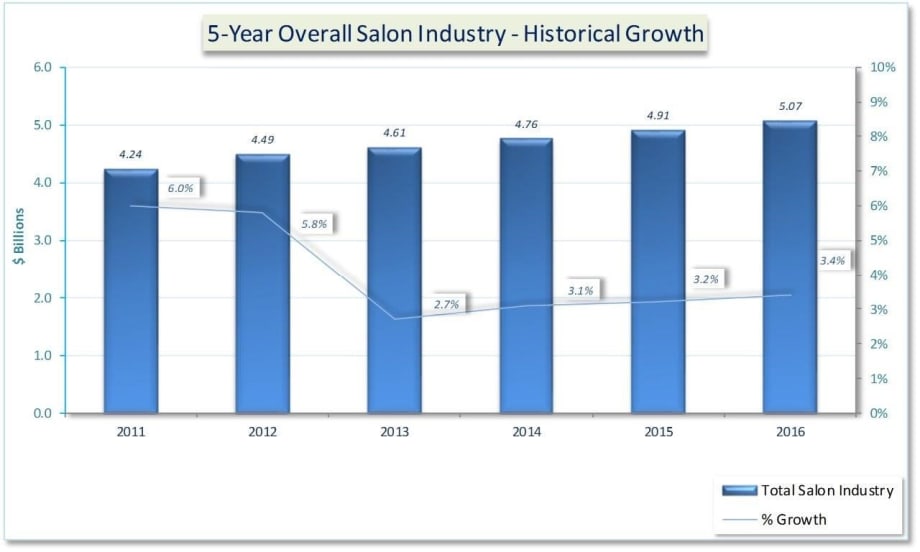

Overall revenues for all salon industry services (hair, skin, nails) plus salon retail grew 3%, per the new 2016 Professional Salon Industry Hair care Study from Professional Consultants & Resources, a leading salon industry strategic consultants and data source.

Total U.S. salon services and salon retail sales grew by 3% to $62 billion. There are nearly 270,000 salons and barbershops in the USA using and selling salon hair care products.

But, the salon count declined by 8.7% as traditional commission based salons closed in large numbers and large rental suites open.

“The state of our salon industry is now in a slow growth mode and is positively trending up,” says Cyrus Bulsara, president of Professional Consultants & Resources. “With the economy trending upwards and issues impacting the salon industry abating, we should see good growth. High performance, innovative new products, better larger salon suites and new management at top manufacturers are key. Sales of hair color, shampoos, conditioners, hair sprays, hair styling products and specialty products all increased. The huge paradigm shift toward large family-economy chains and rentals continues. Rentals still do not retail efficiently and consequently product sales at mega-salon stores like ULTA increase sharply. Some premium hair care lines now sell at high-end beauty specialty, plus department stores, and also on Amazon.”

Haircoloring still remains the vital “Anchor Service” at salons across the USA, bringing in clients for all other services like cuts, styles, perms, straightening etc. Haircoloring services were up nearly 3.6%, equally due to baby boomers needing gray -coverage and the huge demand for fashion hair color, including blonding, highlights, baby-lights, balayage, ecaille, ombré/sombré. Vibrants, vivids and pastels are slowing. Keratin straightening and perms grew 2%. Cutting and styling grew at 2.8%, as client visits to salons increased slightly, with better incomes.

Major highlights of the study include:

The study analyzes the robust growth of men’s salon services and product sales in great detail. Men’s haircolor grows strongly.

Traditional independent salons and mid-tier mall chains close, giving way to family-economy chains and suite rentals, plus high-end men’s barbershops. This is a huge and dynamic market trend, quantified and analyzed in detail, to further client sales and education of rentals.

At the two major U.S. distributor groups: BSG/CosmoProf sales were up 5.5%. Sales at L’Oréal’s SalonCentric were in flat to low growth.

Sally Beauty store sales were up 1.9%, despite major economic headwinds on disposable incomes, especially in calendar 4Q 2016.

Better independent salons, and A and B class rentals, drive full-service sales at CosmoProf, SalonCentric and other distributor stores.

Top suite rental organizations like Sola, Salon Plaza, Salon Lofts, Solera, Phenix, Salons by TJ and Salon Concepts continue rapid growth.

Sales at Regis are still not stabilized, as they study divesting high-end brands, and attempt franchising value brands, plus study rentals.

Great Clips and Sport Clips both registered 9.4% and 15% growth, respectively. These two family-economy chain franchises are extremely well run and grow at multiples of the entire industry’s service growth rates.

Styling product sales increased by mid-single digits, as clients rely on home hair styling with new genres of more efficient styling tools.

Specialty products, including hair loss, shine, thermal protection, oils etc. grew rapidly at nearly 7%, led by sales of various natural oils.

Sales of shampoos and conditioners grew at low single-digits, as women shampoo less often and use cheaper mass-retail brands.

Salon retail care grows mainly due to hair color protection and new genres of hair/scalp masks, massage, treatments and protein infusion.

At ULTA, salon products grew at about 15%, mainly due to their aggressive seasonal promotions and special offers with deep discounts.

Direct sales at Wella Intl., Aveda, Kerastase and Bumble all grew. Wella had the strongest growth, due to new brands and the best education.

Redken and John Paul Mitchell Systems, were the only two major companies with mid-single digit growth, due to their innovative new launches.

Market shares are detailed for every company, with L’Oréal Professional, Coty Professionals and John Paul Mitchell Systems, respectively, ranked as the top three manufacturers.

Henkel vaults into fourth rank with Schwarzkopf, Sexy Hair, Kenra and Alterna.

Estée Lauder with Aveda and Bumble ranks next.

Unilever (TIGI and Alberto-Culver), Shiseido (Joico and Zotos), Revlon Professional (American Crew, Roux), and KAO (Goldwell/KMS) follow.

Luxury Brand Partners and Keune Haircosmetics USA, both achieved double-digit growth. Keune leverages off a small base with new distribution. LBP and Kevin Murphy are two, new, high-growth players in the premium segment.

NEW sections detail cut, color and style trends; data analysis of barbershops and men’s services/products; ingredient issues; leading manufacturers’ reps; plus, sales data for AG Hair, Aloxxi, Alterna, Bio Ionic, Brazilian Blowout, Cadiveau, Peter Coppolla Beauty, Phyto, Davines, IT&LY, Framesi, GK Hair, Kenra Professional, Keratin Complex, Keune, Marcia Teixeira, Phyto, Pravana, Scruples and many more.

The study features highly detailed illustrative graphs/charts making data user-friendly.

For purchasing, further info., or any questions, contact cyrus.bulsara@ProConsultants.us